Biometric authentication and alternative credit scoring at scale (GDP Labs)

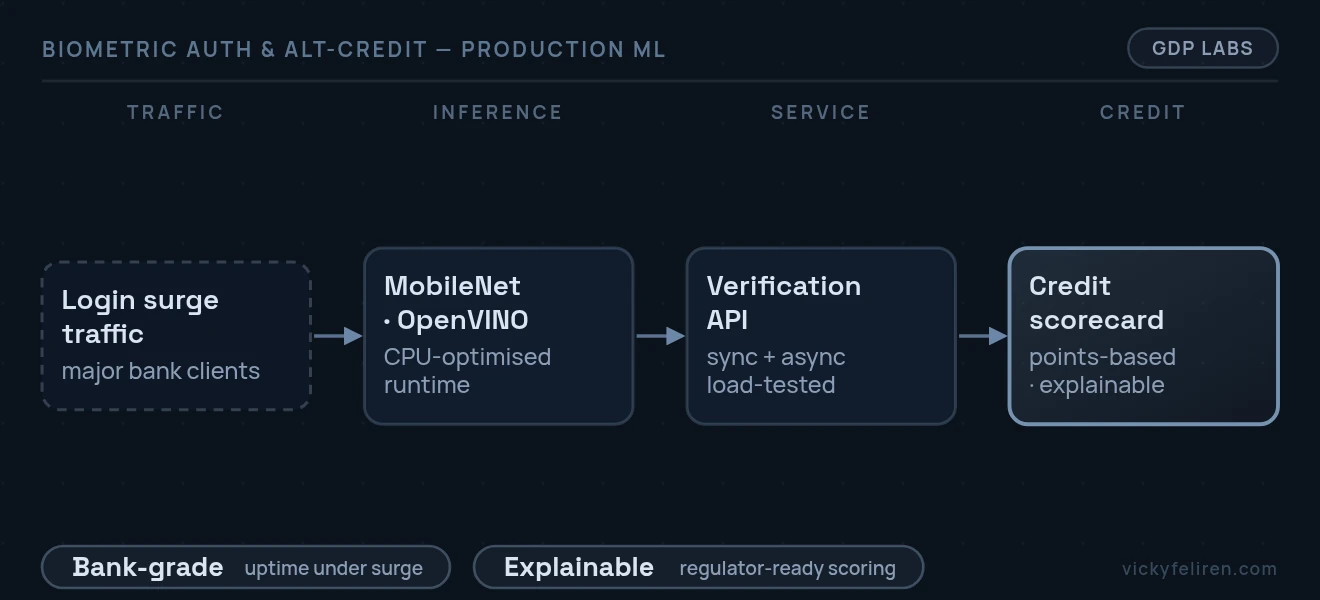

A major Indonesian bank required a production-grade biometric authentication stack capable of handling login surges at national scale, while simultaneously needing to expand credit access to "thin-file" borrowers, individuals with insufficient traditional credit bureau history to receive a FICO-equivalent score under conventional underwriting. Indonesia's fintech regulator OJK requires full model explainability and fairness documentation for any credit scoring model deployed in a regulated lending product.

Biometric systems for financial services face an adversarial threat model. Presentation attacks (photo prints, video replay, 3D masks) are economically motivated at this scale. Anti-spoofing and liveness detection must operate at CPU-only inference (no GPU in production banking infrastructure at the time) under a strict latency SLA at 1M+ daily inferences. Credit scoring under OJK mandates that the model be interpretable to a non-ML-specialist regulator, which rules out standard gradient boosting outputs without explicit explainability transformation and requires documentation of fairness analysis across demographic groups.

Deployed MobileNet backbone (optimized for CPU inference) under Intel OpenVINO runtime, achieving 90% verification accuracy at 99.99% uptime through login surge peaks of 1M+ daily inferences. Designed synchronous and asynchronous load testing harnesses in JMeter to establish production latency benchmarks and identify bottlenecks before deployment. Anti-spoofing and active liveness modules tested under both sync/async load profiles.

All credit scoring experiments tracked with MLflow (hyperparameter logs, model registry, metric versioning). Shipped a regulatory-explainable scorecard model, a logistic regression converted to a points-based scorecard format interpretable by OJK auditors, with SHAP-based feature importance documented for the fairness review. Alternative data signals used: transaction history patterns, behavioral metadata, and device signals for thin-file borrowers previously excluded from formal credit markets. Validated against a 6-month client-monitored window, delivering 35% higher loan approval efficiency and a 25% lower default rate vs. prior baseline.

Established reproducibility standards (fixed seeds, version-pinned configs, regression benchmarks) adopted across 5+ products. Built scalable serverless clustering API on AWS (Kubernetes, scikit-learn, MLflow) for an analytics platform, 40% increase in business leads reported by client. Set internal code-review bar and automated ML pipeline standards that reduced research-to-production handoff friction company-wide.

Led HR analytics initiative using PrestoDB and Metabase, resulting in 50% productivity measurement improvement for internal operations team.

Expanded financial access to thin-file borrowers previously unscoreable by traditional credit bureaus, while maintaining full OJK regulatory compliance. Biometric stack protected millions of users from presentation attacks at 99.99% availability, a reliability standard equivalent to Tier 4 data center SLAs applied to an ML inference service.